axis payroll User Guide Supplement March 2022 |

||

1. What's New? |

||

|

||

1.1 Employer Bulletin February 2022 |

||

|

You are advised to read the Employer Bulletin: February 2022 which is available from the GOV.UK website |

||

1.2 P60 Stationery |

||

|

Employers continue to be required to supply all employees with a P60 if they are still in your employment at the end of each tax year. HMRC are no longer supplying pre-printed stationery. axis payroll prints the P60 documents to a PDF file from where the documents can then be printed on plain A4 paper and issued to your employees. Note: for axis payroll 2020 users or those that have the Paperless Payroll Foundation feature, running Create P60 Atttachments will create an axis payroll password protected pdf version of the P60 on the employee record. Additionally, for axis payroll systems with the People HR Interface feature or the eDoc Deposit Interface feature, P60's can be delivered to your employees via their People HR or eDoc Deposit account. These are password protected and an additional password protected copy is stored in the attachments tab of the employee record in axis payroll.

|

||

1.3 Health and Social Care - NI Contribution Increase |

||

|

On 7th September 2021 the government announced a new 1.25% Health and Social Care Levy to fund investment in the NHS, health and social care. The Levy is effectively introduced from April 2022 when National Insurance contributions for working age employees, self-employed people and employers will increase by 1.25 percentage points. In the December 2021 Employer Bulletin, HMRC asked employers to include a message for employees on all payslips between 6 April 2022 and 5 April 2023 to explain their increased National Insurance contribution. The message should read: “1.25% uplift in NICs funds NHS, health & social care.” axis payroll 2016, 2018 and 2020 will include this message on A4 payslip formats (AXIS9 and Plain A4) but is unable to include this message on other payslip formats. All other payslip formats will also be discontinued from axis payroll from 6th April 2023. From April 2023, the Levy will be formally separated from National Insurance contributions and will also apply to the earnings of individuals working above State Pension age. National Insurance contribution rates will then return to 2021 to 2022 levels. The axis payroll March 2023 year end update software release will include modifications to handle the new levy and details will be included in the documentation released for March 2023.

|

||

1.4 Freeports Employer National Insurance Contributions Relief |

||

|

The government has announced that Employer National Insurance contributions (NICs) are to be included in the wider Freeports initiative. Employers with business premises within a Freeport tax site will be able to apply a zero-rate of secondary Class 1 National Insurance contributions on the earnings of new employees who spend 60% or more of their working time within the tax site. This rate can be applied on the earnings of all new hires up to £25,000 per annum for 36 months per employee. Governement guidance will be available for employers to self-assess eligibility to claim this relief. This change in rate would see all employers based within and employing people working within the Freeport geographic area, apply a zero-secondary rate of employer NICs for such employees’ earnings above the secondary threshold up to and including a new Freeport Upper Secondary Threshold (FUST). |

||

1.5 National Insurance Holiday For Employers Of Veterans |

||

|

Introduced on 6 April 2021, employers who hire former members of the UK regular armed forces during the first year of their civilian employment will be eligible for a zero-rate of secondary National Insurance contributions for up to 12 months up to the Veterans Upper Secondary Threshold. Employers will be able to claim this relief through Real Time Information submissions from 6 April 2022 and any earnings of qualifying veterans hired from 6 April 2021 will be eligible for retrospective National Insurance contributions relief. HMRC guidance is now available for employers wishing to take advantage of the National Insurance holiday for employers of veterans. |

||

1.6 Parental Bereavement Leave and Pay in Northern Ireland |

||

|

A new right to Parental Bereavement Leave and Pay comes into force in Northern Ireland 6 April 2022. This will mirror the parental bereavement provisions that have been in place in Great Britain since April 2020. axis payroll already supports the recording of Parental Bereavement Leave and the processing of Statutory Parental Bereavement Pay (SPBP). |

||

1.7 Increase to Employment Allowance from 6th April 2022 |

||

|

As announced by the Chancellor of the Exchequer 23rd March 2022 in the Spring Statement 2022, the annual Employment Allowance increases for eligible businesses from £4,000 to £5,000 from 6th April 2022.

|

||

1.8 National Insurance Primary Threshold Increase from 6th July 2022 |

||

|

As announced by the Chancellor of the Exchequer 23rd March 2022 in the Spring Statement 2022, the level at which employees start to pay National Insurance contributions will increase through the application of a raise to the National Insurance Primary Threshold from £9,880 per annum to £12,570 per annum from 6th July 2022. axis payroll will be updated to reflect these new thresholds in the coming weeks and customers will be contacted and advised to install a payroll software update to implement these changes during June 2022. Further documentation relating to these changes will also be published at that time. |

||

2. Information for axis payroll 2016 and axis payroll 2018 users

|

The document below is not the latest version. To see the latest version, please click here. |

The information contained in this Payroll User Guide Supplement applies to axis payroll 2016, axis payroll 2018 and axis payroll 2020 users. axis payroll 2016 will not be supported to run the 2022/2023 payroll year end. Please complete an Upgrade Request as soon as possible if you are still running axis payroll 2016.

3. Preparation

|

|

The document below is not the latest version. To see the latest version, please click here. |

3.1 When Do I Install the Update?

Your axis payroll software must be updated before you will be able to perform the payroll 2021/22 year end.

You do not need to install this update until you have completed the final period of the year, however it is safe to install the update at any time.

3.2 Dates Of Birth

In order to allocate employees to the correct NI category, you must ensure that you hold the correct date of birth against each active employee record.

3.3 Employee Addresses

In order for HMRC to apply Scottish Rate of Income Tax and Welsh Rate of Income Tax correctly, it is important that employee addresses are kept up to date.

3.4 Employer Bulletin

You are advised to read the Employer Bulletin: February 2022 which is available for download from the GOV.UK website.

3.5 Year End Stationery

P60 bulk stationery was withdrawn by HMRC in 2021. P60's are printed to PDF for printing and distribution to your employees unless you are using our supported Paperless Payroll interfaces.

3.6 P45 Stationery

Similar to the P60, bulk stationery for P45 was withdrawn by HMRC in 2021.

P45's are now printed to PDF.

3.7 Week 53 / Week 1

The 2021/2022 tax year includes a Week 53 for weekly payrolls where the pay date lands on 5th April 2022.

4. Installing the Update

|

|

The document below is not the latest version. To see the latest version, please click here. |

4.1 Where Do I Install The Update?

The update must be installed on your axis payroll software server. This will usually be your network server, but a number of axis payroll users run their payrolls on a stand-alone PC.

4.2 Downloading the axis payroll software update

If you have the axis diplomat accounts package installed on the same server as your payroll, you can schedule a full axis diplomat software update from within axis diplomat for automatic overnight installation. Instructions on scheduling a software update can be found at Scheduling an axis diplomat software update

Alternatively, customers will manually download the update from our website as in previous years.

To manually download the update:

- Ensure you are logged on to your payroll server as an administrator.

- Ensure you are logged into your account at www.axisfirst.co.uk.

- Your software update can be downloaded from https://www.axisfirst.co.uk/payroll-march-2022 then selecting the appropriate download. Ensure that you read the terms and conditions fully before proceeding; an option is provided to print these if required. This area provides full instructions on installing software updates.

4.3 Installing the Update

Follow the Installation Procedure detailed below.

Please note that you need only install this update once for all axis payrolls providing that all payrolls reside on the same machine. Where payrolls are 'switched' between 'home' and 'office', then each such machine requires the update.

4.3.1 Copy Data to Full Backup

Ensure that a full backup of the system is taken. Use the 'Copy Data to Full Backup' function to create an archive backup of the payroll data on to removable media. We also strongly recommend that a full backup of the axis programs and data is made.

4.3.2 Installing the Update

You should run the installation procedure from the axis payroll server.

- You should be logged onto the axis payroll server. Elevation will be required.

- Ensure that all axis users are out of the system. You can do this by clicking on the System Console/User Status Enquiry button, found on the axis payroll Scheduler toolbar. Then come out of the system yourself

- If installing a downloaded version of the software, the file needs to be on the axis server and so may need to be copied to the server either directly over the network or via a form of removable media if it has been downloaded on another workstation. The executable can then be run to install the update files.

- If installing from removable media, insert the update device into the server. The device should auto-run. If it does not, please call for assistance

- Click on Install/Upgrade axis diplomat (2016, 2018 or 2020) System.

- Click Upgrade Existing System.

- If you are continuing to use axis payroll 2016 or 2018, an information screen will appear:

Confirm that you wish to continue- Confirm that you accept the terms of the license agreement:

- Select the drive that contains your axis payroll system. This will normally be the default drive presented:

- The installation procedure will now check that there are still no users in the system, check for sufficient disk space and then ask you to confirm that you wish to update the axis diplomat Software.

- The installation procedure will continue and update the axis payroll software.

- Once the installation has completed, you will receive a ‘Setup Completed Successfully’ message, click ‘OK’ and then ‘Cancel’ out of the menus.

- Finally, whilst you are still logged on to the axis server, you should enter each of your axis payroll systems in turn and perform any updates requested.

- This completes the installation procedure. Once the installation has completed, you will receive a ‘Setup Completed Successfully’ message, click ‘OK’ and then ‘Cancel’ out of the menus.

5. Claiming Veteran NIC Relief For 2021/2022 Tax Year Through Payroll

5.1 Overview

As described in the What's New? section of axis payroll User Guide Supplement March 2022, a 12 month National Insurance holiday for employers of veterans was introduced from 6th April 2021 however the relief could only be claimed through Real Time Information submissions from 6th April 2022 with any earnings of qualifying veterans from 6th April 2021 onwards being eligible for retrospective National Insurance relief. Guidance on claiming the relief is available from HMRC at https://www.gov.uk/guidance/claim-national-insurance-contributions-relief-for-veterans-as-an-employer.

If you wish to claim this relief through RTI you will need to follow the instructions below on or after 6th April 2022 after running your final period end for tax year 2021/2022 but before running your final Calculate Monthly Remittance and proceeding with the year end processes detailed in section 6 of this user guide.

5.2 Instructions

Calculate the value of Earnings and National Insurance contributions which are eligible for zero-rating of secondary National Insurance contributions during tax year 2021/2022 for each veteran using the N.I.C. Year to Date Report.

Use National Insurance Adjustments to reduce the current employee NI category by the values calculated above.

Use Amend Employee NI Category to select category V.

Use National Insurance Adjustments to enter the required Year To Date Totals for category V.

If applicable, i.e. if 'Veteran employment start date' was before 6th April 2021, use Amend Employee NI Category to reset the category.

Run Calculate Monthly Remittance to incorporate adjusted totals.

Use Create RTI Full Payment Submission and Submit RTI Full Payment Submission to send adjusted year to date totals to HMRC. Note: this submission may not be made before 6th April 2022.

6. Year End Procedures

|

|

The document below is not the latest version. To see the latest version, please click here. |

Ensure that you have installed your axis payroll Legislation Update before proceeding with the year end procedures. Please ensure that a FULL security backup is taken of the payroll data BEFORE installing the axis payroll Legislation Update and again before running the last function ‘Year End Processing’.

You also need to ensure that you have:

- Run your final period end

- If required, followed the procedure for Claiming Veteran NIC Relief for 2021/2022 Tax Year Through Payroll as detailed in Section 5.

- Run 'Calculate Monthly Remittance'

- Checked that your last submitted FPS is correct.

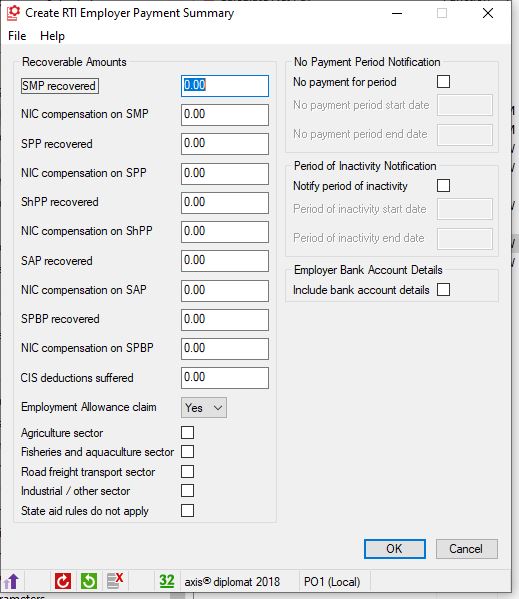

- Created and successfully submitted your final 'RTI Employer Payment Summary' (EPS) if this is your only payroll frequency and payroll data set or is the payroll frequency/payroll data set from which you have chosen to submit combined figures. You will need to submit a final year end EPS even if you have no statutory payments to recover in order to advise HMRC that you are making the final submission for the year.

Please note: HMRC accept the 'final submission for the year flag' in either the last submitted FPS file for the year or in the final EPS file. axis payroll only supports submission of this flag in the EPS and the file is automatically flagged in the background as the final submission for the year. Refer to http://www.gov.uk/payroll-annual-reporting/send-your-final-payroll-report for further information.

6.1 Reports to Run

6.1.1 Print Pay Component Year End Totals

The system will produce a 132 column plain paper report detailing the total amounts accumulated for each pay/deduction component, total PAYE and total NIC. Please read the associated help documentation for further details.

6.1.2 N.I.C. Year to Date Report

The system will produce a 132 column plain paper report (based on the NIC section of a P11) detailing N.I. Liable Earnings and N.I. Contributions for each employee on a period by period basis for the frequency selected.

We would advise that the report is kept for a minimum of 3 years, in case of query from HM Revenue & Customs.

Please read the associated help documentation for further details.

6.1.3 P.A.Y.E. Tax Year to Date Report

The system will produce a 132 column plain paper report (based on the PAYE section of a P11) detailing Taxable Earnings and Tax Paid for each employee on a period by period basis for the frequency selected.

We would advise that the report is kept for a minimum of 3 years, in case of query from HM Revenue & Customs.

Please read the associated help documentation for further details.

6.1.4 Year End Employee Absence Report

The system will produce a 132 column plain paper report with one page per employee showing each day of sickness absence, maternity leave, etc, taken during the year. Both April 2021 and April 2022 are printed for information.

Please read the associated help documentation for further details.

6.1.5 Year End Payment Summary Report

The system will produce an 80 column employee listing of NIC and tax deductions followed by a summary of payments for the year.

We would advise that a copy of the report is kept on file for a minimum of 3 years in case of query from HM Revenue & Customs.

Please read the associated help documentation for further details.

6.2 P60 Print

A P60 must be generated and delivered to each employee still employed on 5th April.

As HMRC have now withdrawn the bulk stationery for P60's and P45's, the P60 will need to be printed to PDF from your axis diplomat payroll system and then printed from the pdf viewer.

The documents are printed in surname order.

Please read the associated help documentation for further details.

For those axis payroll systems with a paperless payroll interface, Create P60 Attachments should be used in preference to the P60 Print function and the attachments should then be uploaded using Deliver P60 Attachments (see section below).

6.3 Create P60 Attachments

The Create P60 Attachments function is available to axis payroll 2020 users or if the People HR Interface or eDoc Deposit Interface features are set and will create a password protected pdf version of the P60 as an attachment on the employee record.

If a supported interface is being used to deliver payroll documents, this function should be used in preference to the P60 Print function. Documents are then delivered to the inteface using Deliver P60 Attachments.

6.4 End of Year Returns

You must ensure that you have successfully submitted an RTI Employer Payment Submission file if this is your only payroll frequency and payroll data set for the employer PAYE reference or is the payroll frequency/payroll data set from which you have chosen to submit combined figures before proceeding to use the Year End Processing function. You will need to submit a final year end EPS even if you have no statutory payments to recover in order to advise HMRC that you are making the final submission for the year.

Please note: HMRC accept the 'final submission for the year flag' in either the last submitted FPS file for the year or in the final EPS file. axis payroll only supports submission of this flag in the EPS and the file is automatically flagged in the background as the final submission for the year. Refer to http://www.gov.uk/payroll-annual-reporting/send-your-final-payroll-report for further information.

7. Year End Processing

|

|

The document below is not the latest version. To see the latest version, please click here. |

7.1 Security Back Up

You should now take a Year End Security Copy of all axis payroll Data using the 'Copy Data to Full Backup' function and selecting the 'Retain backup indefinitely' and 'Archive backup' options.

We would advise you to keep the backup archive for a minimum of 3 years in case of query from HM Revenue & Customs.

This is also important in case there is a problem with your end of year returns.

7.2 Year End Processing

This function needs to be run for each payroll frequency.

The system asks for confirmation that you have read and understood this guide before proceeding and that a security back up has been taken.

The process then clears all accumulators to zero for the new tax year.

The previous years’ details are retained in the Payroll Payment Archive File.

The Employment Allowance tick box located in Amend Employer Details is automatically cleared if your Employers National Insurance for tax year 2021/2022 exceeds £100,000.

Re-enter your payroll system.

8. The New Year

|

|

The document below is not the latest version. To see the latest version, please click here. |

8.1 Employment Allowance

The Employment Allowance increases from £4,000 to £5,000 per year from 6th April 2022.

Even if you were eligible for, and claimed, Employment Allowance for the tax year ending 5th April 2022, you will need to submit a fresh claim.

If you have are newly eligible to claim the 'Employment Allowance' you will need to go to 'Amend Employer Details' for the payroll data set through which you wish to claim the allowance and tick the 'Employment Allowance' option. Note: if you are operating more than one payroll data set, you should only claim through one data set. Calculate Monthly Remittance will then include your claim for the allowance.

You will also need to create and submit an RTI Employer Payment Summary in the first month of the tax year to advise HMRC that you are claiming the allowance by setting the 'Employment Allowance claim' option to 'Yes' and ticking the appropriate company sector option for your business (see https://www.gov.uk/guidance/changes-to-employment-allowance for further information).

8.2 Tax Code Changes

The standard personal allowance remains at £12,570. This applies to England and Northern Ireland, Scotland and Wales.

The code for standard / emergency use with effect from 6th April 2022 is 1257L.

Tax Code Uplifts are as follows:

- L: N/A due to no change in the Personal Allowance

- M: N/A due to no change in the Personal Allowance

- N: N/A due to no change in the Personal Allowance

Where you receive a code notification for an individual employee to be operated from 6th April 2022 on Form P9(T) or via your online HMRC account, the specified code must be entered after the year end has been run.

Refer to form P9X(2022) for further details.

8.3 Class 1 National Insurance Contributions

Calculate Net Pay will check the tax year / pay date and automatically apply the following Class 1 earnings thresholds effective from 6th April 2022:

| Weekly | Monthly | Yearly | |

| Lower Earnings Limit | £123.00 | £533.00 | £6,396.00 |

| Primary Threshold | £190.00 | £823.00 | £9,880.00 |

| Secondary Threshold | £175.00 | £758.00 | £9,100.00 |

| Freeport Upper Secondary Threshold | £481.00 | £2,083.00 | £25,000.00 |

| Upper Secondary Threshold (Under 21) (UST) | £967.00 | £4,189.00 | £50,270.00 |

| Apprentice Upper Secondary Threshold (Apprentice Under 25) (AUST) | £967.00 | £4,189.00 | £50,270.00 |

| Veterans Upper Secondary Threshold | £967.00 | £4,189.00 | £50,270.00 |

| Upper Earnings Limit | £967.00 | £4,189.00 | £50,270.00 |

In line with the previously announced additional 1.25% Health and Social Care contribution,the Employee Class 1 NI contribution rates for NIC categories A, B, C, H, J, M and Z increase by 1.25 points for earnings above the primary threshold.

Additional National Insurance categories have been added for:

F - Freeport

I - Freeport - married women and widows reduced rate

L - Freeport - deferment

S - Freeport - state pensioner

V - Veteran

The Class 1 National Insurance rates are available at https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2022-to-2023

Calculate Gross Pay will continue to check employees in the 'under 21' and 'under 25' N.I. categories and amend their category to a standard category if that employee has achieved the age of 21 or 25 by the pay date of the period being run.

Note: The 'Print Payroll Parameters' function, accessed from the 'Supervisor Functions' menu, may also be used to produce a report of the rates applicable to each NI category and band of earnings.

8.4 Statutory Sick Pay

The weekly rate increases to £99.35.

The appropriate daily rate is determined by the number of qualifying days.

Eg. The daily rate for an employee with five qualifying days is £19.87.

8.5 Statutory Maternity / Paternity / Adoption / Shared Parental and Parental Bereavement Pay

Statutory Maternity Pay (SMP) and Statutory Adoption Pay (SAP) are paid at 90% of the employee's average weekly earnings for the first six weeks. The standard weekly rate for the remaining weeks is £156.66 or 90% of the employee's average weekly earnings, whichever is lower.

Statutory Paternity Pay (SPP) is payable for 1 or 2 weeks at the standard weekly rate of £156.66 or 90% of the employee's average weekly earnings, whichever is lower.

Statutory Shared Parental Pay (ShPP) and Statutory Parental Berevement Pay (SPBP) are payable at the standard weekly rate of £156.66 or 90% of the employee's average weekly earnings, whichever is lower.

The amount of SMP/SPP/ShPP/SAP/SPBP that may be recovered for employers who do not qualify for Small Employers Relief (SER) is 92% of the SMP/SPP/ShPP/SAP/SPBP paid to their employees.

Employers who do qualify for Small Employers Relief (SER) can recover 100% of the SMP/SPP/ShPP/SAP/SPBP paid to their employees plus NIC compensation of 3%.

A ‘small employer’ is one who paid (or was liable to pay) total gross class 1 NICs of £45,000 or less in the individuals qualifying tax year. For further information please refer to https://www.gov.uk/recover-statutory-payments

8.6 Student Loan and Postgraduate Loan Recovery

The annual employee earnings threshold for the collection of existing Plan 1 Student Loans increases to £20,195.

The annual employee earnings threshold for the collection of Plan 2 Student Loans remains at £27,295.

The annual employee earnings threshold for the collection of Plan 4 Scottish Student Loans increases to £25,375

The deduction percentage rate for student loans remains unchanged at 9% of earnings above the threshold.

The annual employee earnings threshold for the collection of Postgraduate loans for 2022/2023 remains at £21,000 and deductions are made at 6%.

8.7 PAYE Income Tax

Calculate Net Pay will automatically apply the appropriate annual tax bands for the tax year / pay date as follows:

|

2022 - 2023 |

||

| England & Northern Ireland Basic Rate | 20% | £1 to £37,700 |

| England & Northern Ireland Higher Rate | 40% | £37,701 to £150,000 |

| England & Northern Ireland Additional Rate | 45% | £150,001 and above |

| Scottish Starter Rate | 19% | £1 - £2,162 |

| Scottish Basic Rate | 20% | £2,163 to £13,118 |

| Scottish Intermediate Rate | 21% | £13,119 to £31,092 |

| Scottish Higher Rate | 41% | £31,093 to £150,000 |

| Scottish Top Rate | 46% | £150,001 and above |

| Welsh Basic Rate | 20% | £1 to £37,700 |

| Welsh Higher Rate | 40% | £37,701 to £150,000 |

| Welsh Additional Rate | 45% | £150,001 and above |

The bands for 2022-23 are effective from the first pay day on or after 6th April 2023.

NB. A report of all the current statutory deduction and payment rates can be produced using the ‘Print Payroll Parameters’ function which is located on the Supervisor Functions menu.

8.8 Pension Scheme Qualifying Earnings

As the qualifying earnings are reviewed annually, please contact your pension scheme provider to see if there are any changes.

If so, this can be changed in Amend Pension Scheme Details.

By law, the total minimum amount of contributions which must be paid into workplace pension schemes increased on 6th April 2019. Employers must make a minimum contribution towards this amount and the staff member must make up the difference. If you decide to cover the total minimum contribution required, your staff won’t need to pay anything.

This table shows the minimum contributions you must pay and the dates when they increased:

| Date | Employer minimum contribution | Staff Contribution | Total minimum contribution |

| Until 5th April 2018 | 1% | 1% | 2% |

| 6th April 2018 to 5th April 2019 | 2% | 3% | 5% |

| 6th April 2019 onwards | 3% | 5% | 8% |

Please see https://www.axisfirst.co.uk/documentation/WorkPlace-Pensions/articles/14043 for detailed information on managing workplace pensions in axis payroll.The staff contribution rate may vary depending on the type of tax relief applied by your scheme. If you are unsure check your scheme documents.

8.9 Payrolling Company Car Benefits

If you are payrolling company car benefits, you will need to update the current car details for each employee to provide the 'Date first registered'.

If the vehicle fuel type is Hybrid, you will also need to complete the 'Zero emissions mileage value'.

These changes need to be made before your first payroll run of the new year.